Bobtail vs. Non-Trucking Liability Insurance: What Is the Difference?

Bobtail insurance and non-trucking liability (NTL) insurance are two of the most confused coverage types in trucking. Both are designed for leased owner-operators, both are relatively inexpensive, and both fill gaps left by the motor carrier’s primary policy. But they cover very different situations, and carrying the wrong one, or misunderstanding which applies, can leave a driver exposed at exactly the wrong moment. This article breaks down what each coverage does, when it applies, and how to decide which one fits your operation.

In this article, we cover:

-

What bobtail insurance covers and when it applies

-

What non-trucking liability covers and when it applies

-

The key differences between the two policies

-

When you might need one, the other, or both

Bobtail vs. Non-Trucking Liability: Side-by-Side Comparison

What Is Bobtail Insurance?

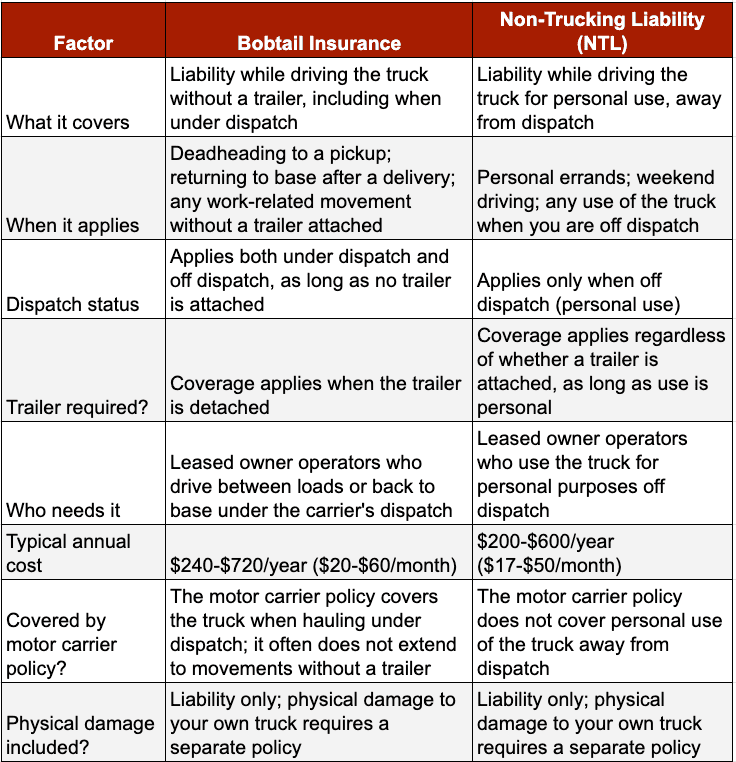

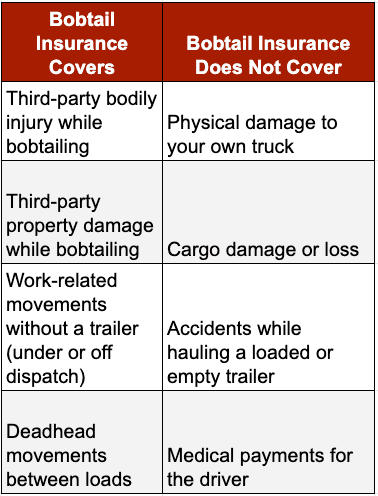

Bobtail insurance covers an owner-operator’s liability when driving a semi-truck without a trailer attached. “Bobtailing” is the industry term for driving a tractor without a trailer; the truck looks like a bobtail cat without its long tail. Bobtail insurance is designed specifically for the gap that exists when a leased owner-operator is moving the truck for work purposes but is not actively hauling a load for the carrier.

The motor carrier’s primary liability policy typically covers the truck while it is under dispatch and hauling a loaded or empty trailer. When the owner-operator drops off a trailer at a shipper’s dock and drives the bobtail back to the yard, or drives to pick up a new load at a different location, the carrier’s policy may not apply. Bobtail insurance fills that gap. It covers liability for bodily injury and property damage to third parties during those work-related movements. It does not cover physical damage to the truck itself, and it does not cover cargo.

What Is Non-Trucking Liability Insurance?

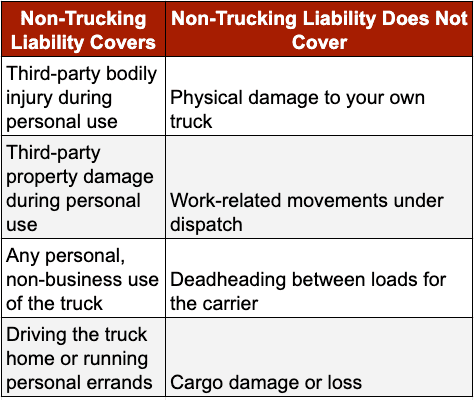

Non-trucking liability insurance covers an owner-operator’s liability when using the truck for personal purposes, away from dispatch. If you drive your semi to run a personal errand, take the truck home for the weekend, or use it for any purpose that has nothing to do with your motor carrier’s business, NTL is what covers you during that time. The motor carrier’s policy applies only when you are working under their authority. The moment you use the truck for personal reasons, that coverage falls away.

NTL is narrower in scope than bobtail insurance. It is designed specifically for personal use, and it does not apply when you are under dispatch. If you are deadheading to pick up a load for the carrier, you are under dispatch, and NTL would not apply to that situation. Some insurers use the terms “bobtail” and “non-trucking liability” interchangeably, which causes significant confusion. Technically, they cover different scenarios, and the language of your specific policy determines which situations are covered.

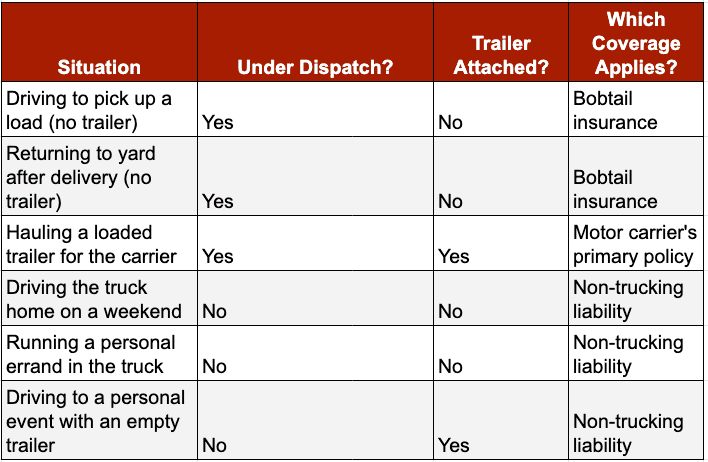

The Key Difference: Dispatch Status

The single most important distinction between bobtail and NTL comes down to dispatch status. Bobtail insurance applies during work-related movements without a trailer, including when under dispatch. NTL applies only when the truck is used for personal purposes, away from dispatch entirely.

Here is a simple way to think about it:

Do You Need Bobtail Insurance, NTL, or Both?

Whether you need one or both depends on how you use your truck when you are off a loaded haul. Most leased owner-operators carry at least one of these two coverage types. Here is how to think through which applies to your situation.

You likely need bobtail insurance if: you regularly drive the bobtail between loads, deadhead to different pickup locations, or move the truck for work purposes without a trailer. This is common for owner operators who are frequently repositioning between runs under dispatch.

You likely need non-trucking liability if: you take the truck home, use it for personal purposes, or operate it for any reason unrelated to the motor carrier’s business. Most leased owner operators fall into this category at some point, even if only occasionally.

You may need both if: you regularly do both, moving between loads under dispatch and also using the truck personally. Many owner operators carry both policies because the combined annual cost is low relative to the liability exposure.

One important note: some insurers offer a single policy that covers both scenarios under one endorsement. Before purchasing separate policies, ask your agent whether a combined option is available and whether it would be more cost-effective for your operation.

Conclusion

Bobtail and non-trucking liability are both small, affordable coverage types that protect leased owner-operators from a large and often overlooked liability exposure. Bobtail covers work-related movements without a trailer. NTL covers personal use away from dispatch. They are complementary, and many operators carry both. The most important step is confirming that your coverage matches how you actually use your truck, so there are no gaps when a claim happens.

Truck Writers specializes exclusively in commercial trucking insurance and can review your current coverage, explain exactly where your motor carrier’s policy ends, and help you decide whether bobtail insurance, non-trucking liability, or both make sense for your operation.

Get a quote here.