Owner-Operator Trucking Insurance: A Complete Guide (2026)

Getting the right insurance is one of the most important financial decisions an owner-operator makes. The wrong coverage leaves gaps that can wipe out a trucking business after a single claim. The right coverage keeps you on the road, satisfies FMCSA and shipper requirements, and protects your income whether you run under your own authority or lease to a motor carrier. This guide walks through everything you need to know to build the right coverage package for your operation.

In this guide, we cover:

-

The types of coverage owner-operators need

-

How coverage requirements differ based on your authority status

-

What each coverage type costs in 2026

-

How to shop for the best rate

Owner Operator Trucking Insurance: Coverage Overview

Step 1: Understand the Types of Coverage You Need

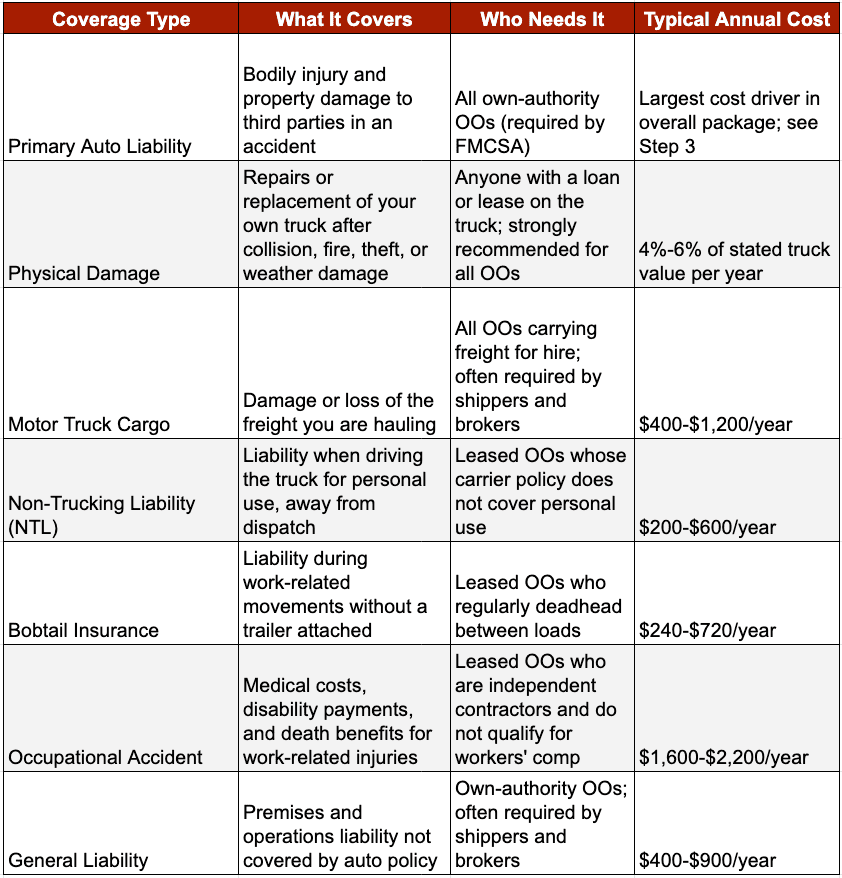

Owner-operator insurance is not a single policy. It is a stack of individual coverages, each one designed to protect against a different type of loss. Understanding what each coverage does is the first step to making sure nothing falls through the cracks.

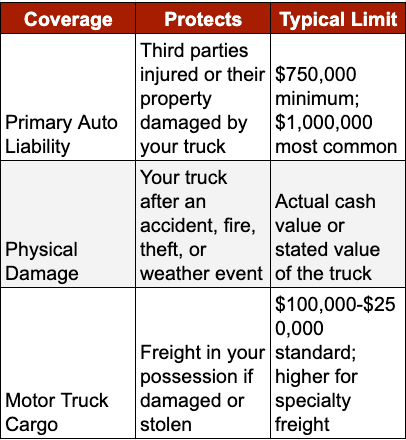

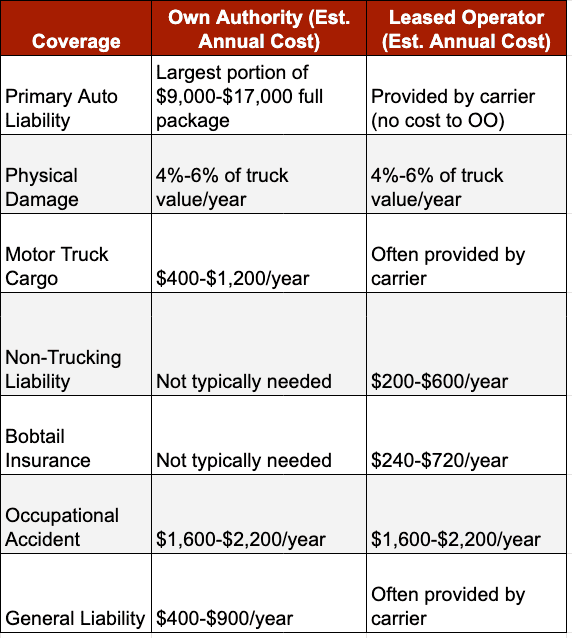

Primary auto liability is the foundation of any owner-operator insurance package. It pays for bodily injury and property damage to other people when you are at fault in an accident. The FMCSA requires a minimum of $750,000 in liability coverage for most freight operations, but most shippers and freight brokers now require $1,000,000 or more before they will work with you. This is the most expensive single line item in an owner-operator’s insurance stack.

Physical damage covers repairs or replacement of your own truck after a collision, fire, theft, or weather event. If you financed or leased your truck, your lender almost certainly requires physical damage coverage as a condition of the loan. Even if you own the truck outright, replacing a $150,000+ asset out of pocket after a total loss is a risk most owner-operators cannot afford to take.

Motor truck cargo pays for damage to or loss of the freight you are hauling. Most shippers and brokers require proof of cargo coverage before assigning loads. Standard cargo limits run from $100,000 to $250,000, with specialty cargo (refrigerated goods, electronics, high-value commodities) requiring higher limits and sometimes specialized endorsements.

Step 2: Determine Your Authority Status

The biggest factor in determining which coverages you need is whether you operate under your own authority or lease to a motor carrier. These two operating models create very different coverage requirements.

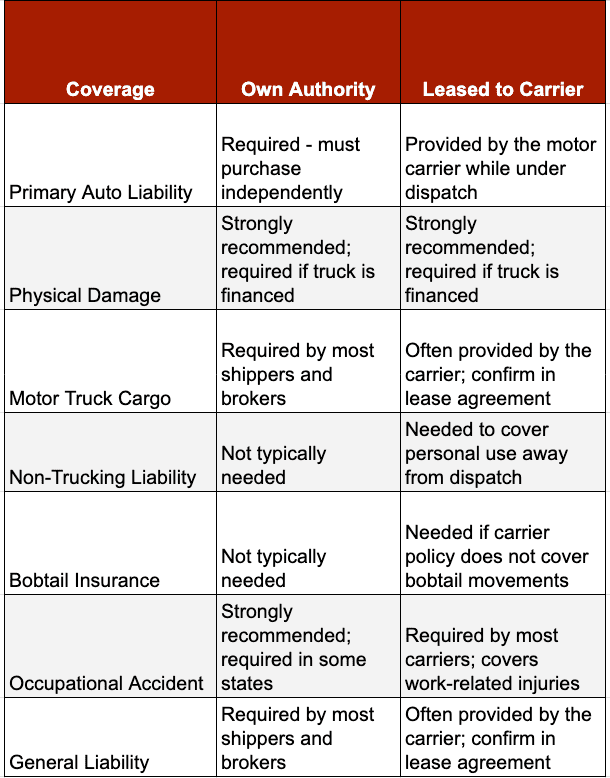

Own-authority owner operators hold their own FMCSA operating authority (MC number) and contract directly with shippers or brokers. They are fully responsible for their own insurance program. This means buying primary auto liability, physical damage, motor truck cargo, and general liability at a minimum. The motor carrier’s insurance does not apply because there is no motor carrier. Own-authority operators also typically need occupational accident or workers’ compensation coverage since they are self-employed and have no employer policy to fall back on.

Leased owner-operators sign a lease agreement with a motor carrier and haul under the carrier’s authority. The carrier’s primary liability policy covers the truck while it is under dispatch. This eliminates the highest single cost in an insurance stack. However, it creates two important coverage gaps: the carrier’s policy typically does not cover personal use of the truck (which requires non-trucking liability), and it may not cover bobtail movements between loads under dispatch. Leased operators also need occupational accident insurance because they are treated as independent contractors rather than employees and therefore do not qualify for the carrier’s workers’ compensation program.

Step 3: Know What Each Coverage Costs in 2026

Owner-operator insurance costs vary based on authority status, hauling radius, cargo type, driving record, years of experience, and the state where you are based. The ranges below reflect 2026 market conditions for established owner-operators with clean records. New authority operators and drivers with violations typically pay more.

Own-authority owner operators pay between $9,000 and $17,000 per year for a full coverage package, according to 2026 industry benchmarks. New authority operators entering the market for the first time often pay considerably more, with primary liability alone running $12,000 to $18,000 annually before adding physical damage and cargo. Physical damage rates are typically calculated as 4% to 6% of the truck’s stated value per year – on a $150,000 truck, that works out to $6,000 to $9,000 annually.

Leased owner operators pay significantly less out of pocket because the motor carrier provides primary liability. A typical leased OO coverage package (physical damage, occupational accident, NTL or bobtail, and cargo if not provided by the carrier) runs $3,000 to $7,000 per year depending on the truck’s value and operating profile.

Step 4: Shop With an Independent Multi-Carrier Agency

How you shop for coverage matters as much as what coverage you buy. Owner operators who work with an independent trucking insurance agency, one that represents multiple carriers rather than a single insurer, consistently access more competitive rates than those who go directly to a single carrier.

An independent agency shops your account across multiple insurance markets simultaneously. Rather than receiving one rate from one carrier, you receive competing options. The agency’s job is to match your specific operating profile (cargo type, hauling radius, driving history, truck value, authority status) to the carrier that offers the best combination of coverage and price for that exact profile. Direct carriers can only offer their own products at their own rates.

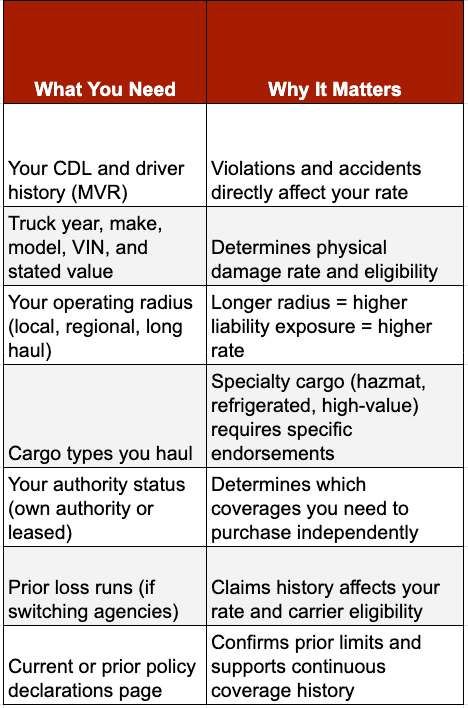

When preparing to get a quote, gather the following information in advance. Having it ready significantly speeds up the quoting process.

Conclusion

Owner-operator trucking insurance is not one-size-fits-all. The right coverage stack depends on your authority status, the freight you haul, how far you drive, and the value of your truck. Understanding what each coverage does, what it costs, and where the gaps are is the foundation for building a program that actually protects your business when something goes wrong.

Truck Writers has specialized exclusively in commercial trucking insurance for over 43 years. Every agent on staff works in trucking and nothing else. Whether you are a new authority operator getting coverage for the first time or an experienced driver looking for a better rate at renewal, Truck Writers can shop your account across multiple carriers and put together the right coverage package for your operation.

To download a copy of this report or learn more about our agency, please reach out here.